There is sufficient evidence to demonstrate the RBA influence over consumer prices is deficient and can produce socially suboptimal policy outcomes. This article provides the reasoning for rejecting the RBA inflation targeting policy and suggests an alternative policy.

The main points:

- There is insufficient evidence to claim that decreasing inflation is caused by increases in the official cash rate.

- The reasons why inflation targeting is not an acceptable policy are explained.

- A suggested alternative is designed around the legislative and fiscal powers of the Australian Government.

Inflation Targeting

The inflation targeting policy (also known as monetary policy) of the reserve Bank of Australia (RBA) policy is to “promote price stability, full employment, and prosperity and welfare of the Australian people.”

Inflation targeting policy can be described in three statements.

- The expected result —

- Increasing the official cash rate (OCR) will result in smaller increases in the consumer price index (CPI) in future periods (decreasing inflation), allowing the OCR to decrease to a neutral rate.

- Is achieved when —

- A neutral interest rate (does not encourage or discourage inflation) and a non-accelerating inflation rate of unemployment (NAIRU) fix changes to the consumer price index to within a preferred range of values.

- Because —

- Expectations of decreasing inflation reduce expected wages growth (wage growth is limited by unemployment equal to the NAIRU) and this in turn reduces price increases (no wage-price spiral).

- Increasing total interest paid by holders of variable rate debt reduces aggregate demand to a level consistent with aggregate supply at full/NAIRU employment (no capacity constraint).

Monetary policy has the advantage of being, a) easy to implement quickly, b) accepted by financial markets, and c) not sensitive to political interference. The latter point means the RBA makes policy decisions independent of government. This independence is sometimes linked to the ‘budget constraint’ conditions of fiscal policy. 1

The Expected Result

There is a lack of evidence supporting statement that increasing the OCR reduces future changes in the CPI. This deficiency results from the OCR being sometimes dependant and sometimes independent of inflation. Also, there is a lack of information on how a change in the OCR actually propagates through the economy over time. How do variables such as unemployment, prices, wage costs and household final consumption expenditure respond to changes in the OCR?

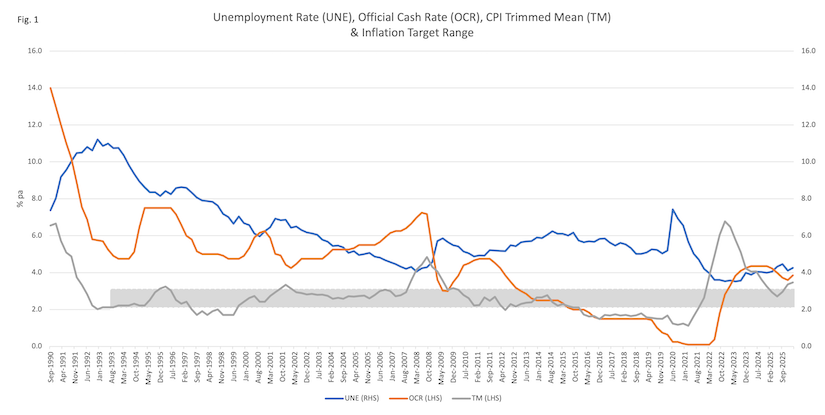

Figure 1 shows the unemployment rate, the trimmed mean CPI and the OCR for the period December quarter 1990 to March quarter 2026.

An increase (decrease) in inflation tends to be followed by an increase (decrease) in the OCR. Sometimes the OCR has decreased while inflation increased (Mar-2001 to Dec-2001), increased while inflation decreased (Jun-2009 to Mar-2011) and remained unchanged while inflation increased (Mar-2021 to Mar-2022). Over the period from Jun-2002 to Sep-2007 the OCR increased by 213 basis points (from 4.27% to 6.4%) and the inflation remained within a one-half percent range (2.58% to 3.07%). 2

There is no unequivocal evidence that an increase in the official cash rate creates decreasing inflation over a given period of time.

Is Achieved When

The neutral (natural) interest rate and the NAIRU are hypothetical, unobservable constructs that are inferred by subjective statements. The values of these key variables can fall within changing upper and lower limits and cannot be precisely estimated from past empirical data. Using past data will not necessarily produce a value optimised for future economic conditions.

The neutral interest rate (defined as a real interest rate) is meant to be high enough to reduce inflation, yet low enough to avoid a recession, over some unknown time frame. It is the real rate of interest when the economy is not being affected by any short-term economic shocks. There are competing conceptual definitions of the neutral interest rate and arguably a difference between a neutral and a natural rate.

Real rates of money values like interest rates can only be calculated post hoc, after inflation has been measured. The usual way of including future risks of inflation or interest rate changes is by subjective estimates of inflation risk and interest rate risk (premia intended to compensate for a fall in the value of money or a lower interest rate than otherwise obtainable).

Any estimate of the neutral rate must be constrained by the lowest market interest rate (e.g. short-term/low-risk debt) and the highest market interest rate (e.g. long-term/high-risk debt), meaning there are two agents actually paying/receiving that particular rate of interest. As the lower and higher bounds move so too would the neutral interest rate, making its estimation problematic and subject to its own upper and lower estimation points. Hence the subjective statement, “If inflation was in the acceptable range and there was no recession, the real interest rate must have been neutral.”

It is not possible to determine the correct monetary policy response without a very good definition of the neutral interest rate and some method for its calculation. To use a neutral interest rate the RBA would have to calculate the real rate for the future, from within a range of estimates, for the appropriate period of time, account for future changes in domestic and international conditions, and include all economic impacts due to changes in fixed and variable mortgage rates, short-term government bonds, long-term government bonds and corporate bonds, all of which have different risk profiles and risk premia.

The long-term decline of interest rates across the major economies in recent decades is noteworthy (Obstfeld, 2025). This shift suggests co-movement despite differences in real exchange rate movements, various risk premia and non-financial barriers. The implication for monetary policy is the possibility that the OCR needs to be much lower in future years.

The NAIRU is derived from the unemployment rate. It can be thought of as an average subject to some adjustments.

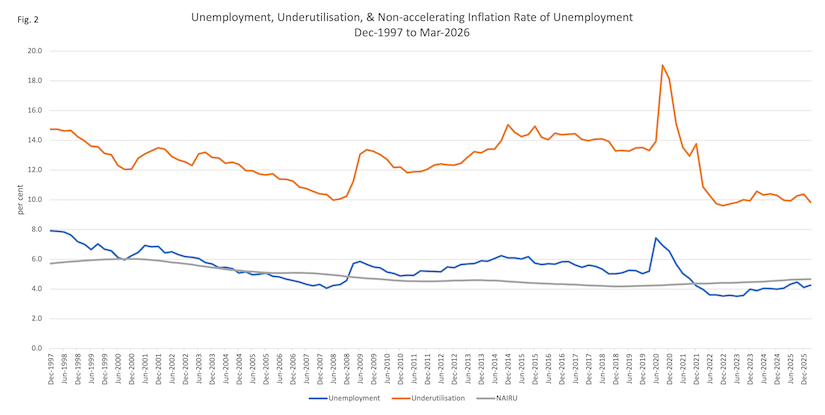

Figure 2 shows the unemployment rate, the broad underutilisation rate and an indicative NAIRU for the period December quarter 1997 to March quarter 2026. 3

Unemployment is relevant to inflation targeting because it reduces the ability of labour to demand wage increases, which would result in higher prices. The NAIRU uses unemployment as a proxy for wage increases and inflationary pressures.

Estimates of the NAIRU can be based on the trimmed mean inflation rate, labour costs per unit, average earning per employee, and the wage price index. Measures of underemployment can be included or excluded. The models commonly used in Australia all produce estimates of the NAIRU within a similar range of values.

Recent data suggests the non-accelerating rates of unemployment are cyclically variant (not the same trade-off all the time) and affected by intertemporal changes in the composition of unemployment (short-term and long-term unemployment and underemployment) over previous periods. There is still a trade-off between employment and prices (lower unemployment with higher inflation), but it varies from period to period. 4. With underemployment relatively higher than unemployment (Fig. 2), estimates of the NAIRU may not be properly capturing any downward pressures on wages.

It is not possible to calculate a definitive value of the NAIRU for the recent past or immediate future. Hence the subjective statement, “If inflation is increasing, unemployment must be lower than the NAIRU.” The correlative statement would be, “If inflation is decreasing, unemployment must be higher than the NAIRU.”

When alternative measures of inflationary pressures, such as the wage price index, or unit labour costs suggest contradictory inflationary pressures the NAIRU is relegated to being just an unemployment definition of full employment.

Because

If wages were continually determined in a competitive market with many buyers and many sellers with unemployment resulting from the labour market clearing at the equilibrium wage, and all prices in the economy were derived from that equilibrium wage, calculating the NAIRU would be easy.

Wages are generally determined from within the labour-enterprise/industry relationships (by institution or legislation), where unemployment and underemployment become conditioning factors. The wage value is relevant to the price setting decisions of companies.

Productivity (multi-factor productivity) is often mentioned in relation to wages, but it is extremely difficult to measure. You can divide the wage cost of a barista by the number of units of output measured in shots of coffee, but it is difficult to measure a unit of labour-capital. Measuring productivity for the non-market sector (no identifiable unit of output) is also a problem.

The mining industry provides an example. A mine with twenty employees processed 1000 tons of ore to produce 10 kilograms of stuff for sale. The high-grade ore was depleted. The twenty employees now process 1000 tons of ore to produce 1 kilogram of stuff. Has productivity increased, decreased or stayed the same?

Productivity changes are not automatically captured by wage increases. This means companies capture by default the bulk of productivity changes and any reduction in real unit labour costs. Under these conditions, company profits would increase relative to wages, and a wage-price spiral is not the most important issue.

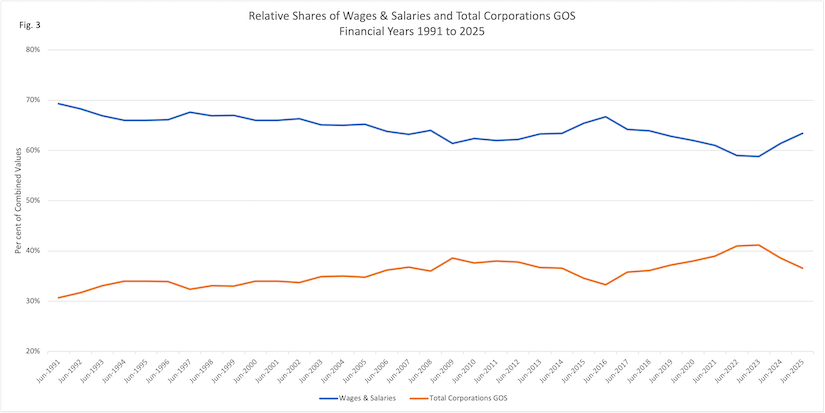

Changes in the relative size of company profits to wages is suggestive of companies being more able to capture income. Figure 3 shows the relative share of wages and salaries has fallen from about 70% to 60% and gross operating surplus has increased from about 30% to 40% over the financial years from 1991 to 2025. 5

The capacity constraint is based on the idea the economy has a long-term potential output determined by the availability of productive resources: labour, new and depreciated capital (buildings, plant, equipment, intellectual property), technological and productivity changes. Short-term deficiencies in these resources have a minor impact on potential output, but long-term deficiencies have a major impact.

The roles of land, water, climate, enforceable property rights, no significant monopoly/oligopoly affected commerce, adequate venture funding, barriers to business, government etc. are assumed or ignored. Increases in potential output from appropriate transport, energy, health, education/training, industrial relations, population and environmental policies are assumed or ignored.

Full employment in this version of potential output is defined in the negative; by unemployment. Unemployment is a long-term deficiency used by the RBA as the rationale for limiting wage growth and creating low and stable inflation. Aggregate demand remains below an employment-based definition of potential output. The NAIRU concept of full employment is maintained by forcing reductions in aggregate demand by increasing the interest payments of mortgage holders.

Unemployed and underemployed persons consume real resources. They want to work (more hours), are actively looking and could start immediately, yet they are unable to fully contribute to the output/income of the economy – actual potential output could be higher. And there are Human Rights issues.

Inflation targeting reduces long-term economic growth by regularly suppressing aggregate demand.

Private sector consumers, particularly holders of variable-rate mortgage debt, take the blame for inflation even though it is unlikely they caused the inflation. Nor is it likely that all companies caused the inflation.

Companies can adjust to short-term changes in consumer demand through inventories or additional labour hours. Additional hours might have higher costs compared to standard hours that can be absorbed by that portion of profits attributable to that production. Companies can use retained earnings. Long-term price decisions are not necessarily affected by short-term inflationary conditions.

RBA Independence

Despite the independence of the RBA, the simplicity and ready acceptance of monetary policy, the RBA should not be indifferent to suboptimal policy outcomes.

Homeowners with a mortgage comprise 35% of households, 32% of households are homeowners without a mortgage and 31% are renters (Source, ABS Census 2025). This means any increase in the OCR directly impacts about one-third of households as consumers. Approximately two-thirds of households are not the subject of an economy-wide inflation policy – for any decrease in inflation, the change in aggregate demand needed from one-third of households must be proportionally larger than that needed from all households. 6

- By requiring a permanent pool of unemployed persons, the RBA commits the government to expenditure for the economic and welfare needs of those persons (healthcare, current and future income support, etc.).

- By affecting the viability of business, some of which close down, the RBA commits the government to lower tax receipts. State, territory and local governments can be similarly affected.

- By increasing business costs through the effects of higher interest rates, and to the extent that higher interest rates increase the incomes/spending of non-holders of mortgage debt, the RBA increases inflation.

- By transferring income from low-income holders of mortgage debt to high-income holders of bank profits (shareholders) and financial assets that benefit from higher interest rates, the RBA is increasing wealth inequality and the social problems caused by that inequality.

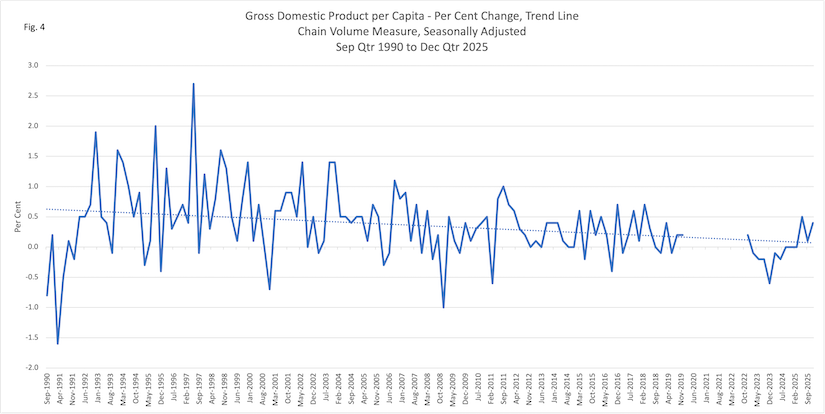

- By suppressing long-term economic growth, the inflation targeting policy could be combining with other domestic and international influences to affect long-term wealth creation. Figure 4 shows the trend of growth in gross domestic product (GDP) per capita has fallen from about 0.5% in September quarter 1990 to about 0.0% in December quarter 2025 (Covid period not shown). 7

Transparency, predictability, consistency and clear communication have not been characteristics of RBA independence. The RBA statements do not provide unequivocal evidence of how or by how much an increase in the official cash rate creates decreasing inflation over a given period of time.

Budget Constraint Conditions

The ‘budget constraint’ conditions legitimately apply to households. When applied to government they are usually stated as:

- Borrowing from the RBA is nil or low: this helps maintain a stable financial environment within which inflation targeting can operate effectively.

- Domestic markets can absorb government debt: government borrowing does not ‘crowd out’ investment of the private sector.

- Taxation provides sufficient funds to meet expenditure: because deficit spending would increase aggregate demand and create inflation, or ‘crowd out’ current consumption and investment to pay for future taxation.

The Australian Government uses fiat currency and an accounting approach based on what actually happens has advantages over theory. The section below describes the operation of fiat money. This section deals with the economic consequences. The important result is that by using fiat money the government can optimise fiscal policy around the use of real resources.

- The Australian Government issues its own currency and has no need to “borrow” from the RBA. The very first job of the RBA is to guarantee no default of an authorisation to pay. A currency issuing government cannot run out of its own money.

- The Australian Government provides a savings product in the form of Australian Government Securities (AGS). The private sector is under no compulsion to “absorb government debt.” The market for AGS is cleared by changes to the interest rate. When the buyers of AGS bid the interest rate up (down), the income of the lender and the government interest payment for that tranche of debt increases (decreases).

- The Australian Government does not need taxation to “provide sufficient funds to meet expenditure.” The alternative condition imposes budget constraint and solvency conditions that require the government budget to tend towards surpluses rather than deficits – just like a private sector household.

The only constraint on government spending is whether or not there are real resources available for use.

The national debt a deficit creates is factually a liability of the government. This liability it is a perpetual, guaranteed, risk-free, interest paying, holding place for large sums of private sector money in a tradeable product (to make a profit) that can be used through RBA open market operations to modify the rate of interest payable.

Private sector saving existing as government bonds does not burden the economy with debt or prevent government expenditures.

In Other Words – We Have

Reductionist Failures

The RBA inflation targeting policy reduces the response to increases in consumer price, whether demand‑side, supply‑side, rest‑of‑world (oil price shocks, military conflict, climate change related reductions in food crops etc.), legislated or regulated, market failure (monopoly/monopsony, cartel, rent-seeking etc.) to subjective judgements about hypothetical, unobservable constructs that cannot have a practical use. The neutral interest rate is essentially a subjective judgement with no practical application. If you consider unemployment and inflation alone, the NAIRU is self-contradicting (has contrary subjective statements). Due to variation from period to period the NAIRU is difficult to calculate and use for future periods.

In response to inflation, the RBA takes action to transfer wealth from mostly mortgage holders to banks and others on the basis this portion of households can influence prices. Mortgage holders and consumers generally do not make price setting decisions.

Price Setting Companies

Companies are ultimately responsible for setting prices. This result is obtained from the fact that perfect competition does not exist in the real world. Companies operate as oligopoly price setters. To generate a profit and obtain a desired rate of return prices must be set at a margin over costs. This margin (mark‑up) might vary with demand, or over time. Prices will change with changes in wage and other costs, productivity, or the mark-up

If the company has sufficient market power (demand does not fall with an increase in prices) the company could increase the mark-up over time to increase the rate of return. The gross operating surplus will grow relative to total wage costs.

Something We Have Learned

Because the neutral rate of interest and the NAIRU are vague by definition and measurement, using past data will not produce values relevant to future inflation. Conditions needed to influence future inflation must be set before the inflation occurs. Setting long-term conditions for low unemployment with socially acceptable constrained wage and price increase will shift potential output towards actual potential output

The burden of inflation targeting falls on a small proportion of households. Most of the impact of increases in the OCR is felt by mortgage holders through higher interest payments to banks. Banks benefit from higher interest income (protecting the real rate of interest and subsequent profit earned).

Fiat Money

Fiat money is not a policy description, just a fact of the Australian Government issuing its own currency. A simplified example presents the characteristics of fiat money.

Money (a medium of exchange) is created when currency ($AUD) is issued by expenditure.

The government decides to spend $300 million on vaccines to be supplied to patients with no out-of-pocket expense. The RBA authorises the bank used by the vaccine company to increase the demand account of that company by $300 million. Later, the Australian Office of Financial Management (AOFM) issues bonds (or notes), known as Australian Government Securities to the same value. These bonds have various values and maturity dates and are bought by many private sector lenders. When the $300 million in bonds matures the AOFM will redeem (repay lenders) and cancel the bonds. The repayment could be financed by using the government’s cash account, subsequent bond issues or another $300 million created by increasing the bank accounts of lenders.

The government has created $300 million by expenditure. The government has removed from circulation $300 million by offering a saving product. The private sector has bought $300 million worth of an interest-bearing risk-free tradeable product.

The government (government/central bank) also ‘destroys’ money. Fiat money is a liability of the government that is destroyed by the accounting removal of the liability from the private sector by taxation, bond sales, RBA open market operations, or private sector debt repayment. 8

The value of money destroyed becomes a value of real resources other economic agents (public and private sector) cannot demand. The government now has the opportunity to demand those real resources for socially acceptable purposes.

Why doesn’t the government just spend as much as it feels like? Because government spending and taxation policy is debated in parliament by elected representatives and subject to commentary of various lobby groups, journalists, or otherwise scrutinised by well-informed and ill-informed persons, society has imposed legislation to control government’s fiscal and monetary decisions.

By issuing debt banks also create money. The debt is a liability (money paid to the debtor) and an equal asset (money repaid by the debtor), which results in no change to equity. A bank with negative equity is insolvent.

State, territory and local governments are similar to households in the sense that a household does not issue fiat money. These levels of government can only spend after they have imposed some fees or charges on persons and business operating within their jurisdiction, or are acting as agents of the Australian Government spending newly issued currency, or otherwise received or borrowed funds. Like households it seems reasonable for these governments to have balanced (own-account) budgets over some number of accounting periods.

Inflation Targeting With A National Taxation Policy

Because the Australian Government issues its own currency, it is able to respond to economic events that require public sector expenditure. Because the Australian Government can destroy money, it is able to release real resources for socially acceptable purposes. Legislative power gives the government an advantage the RBA does not have.

A National Tax Base

For the purposes of this article considerations are, a) simple to understand and apply, b) minimise distortions and inefficiencies, c) equality and equity, and d) not sensitive to political interference.

Sources of market distortion such as stamp duties and payroll fees could be removed. By removing costs not related to a specific input such as labour, materials, energy, plant and equipment the total production cost per unit of product can be reduced. (A range of taxes e.g. land tax, could be reformed into a national tax base. Any reduction in cash revenue affecting state, territory and local governments could be managed by Australian Government expenditure and taxation.)

For this article, comments are limited to, a) personal income tax, b) company income tax, c) super-profits company income tax, and d) goods and services tax (GST).

Personal income tax rates should be progressive (higher income, higher marginal rate) and have enough tax brackets to help reduce the impact of bracket creep (an out-of-scope topic) and still be simple.

The company tax rate should apply to all non-labour (personal) income sources, such as realised capital gains and income from residential property services. This helps reduce distortions of asset values across different classes of assets – important for the efficiency of the tax system.

A permanant non-deductible super-profits tax will not disincentivise companies from earning very high rates of return, but it will allow the government to provide targeted cost-of-living relief when needed. The tax would apply to companies above a certain value of turnover and/or where measures of market concentration and dominance indicate non-competitive conditions.

The GST should apply to all goods and services. The GST should be set at a low rate to reduce the regressive impact. Compensation for low-income earners can be provided through personal income tax offsets or the level of the first personal income tax bracket.

Modified tax rules should apply to superannuation, but that topic is not part of this article.

A Possible Alternative to RBA Inflation Targeting

Changes in interest rates will remain a feature of periods of increasing inflation. There is no impediment to a bank changing a variable interest rate when allowed by a contract – even if the initial rate includes a premium for inflation risk.

An alternative policy needs to condition wage increases and price increases. There are a couple of different ways this might be achieved.

A national tripartite authority of employee, employer and government representatives could determine indicative or benchmark wages for, a) changes in multi-factor productivity, and b) cost-of-living increases, hearing arguments from expert parties. This authority would aim for wages and company profits having long-term sustainable shares of national income. The determinations of this authority would inform industry/enterprise agreements.

No suitable policy exists to condition prices from the supply side. Price controls create distortions and inefficiencies. There is one policy that would condition prices. There are two possibilities that would result in a change in demand companies would notice.

The Australian economy is characterised by a few very large companies in some industries. Economic theory and empirical evidence demonstrate a market with many competitors has better price outcomes. A policy to limit non-competitive markets is imperative.

A temporary increase in the GST would increase prices effectively reducing real incomes and thus reducing aggregate demand. Here, the difference from RBA inflation targeting policy is a reduction of aggregate demand for all households. Additional revenue will allow the government to provide targeted cost-of-living relief.

The problem with any increase in the GST is the effect on the consumer price index. For this reason, having all consumer products include a GST component it is easier to derive a modified consumer price index. The Australian Bureau of Statistics would be producing a consumer price index, a cost-of-living index and an inflation policy index.

A temporary increase in compulsory superannuation contributions from the employee component has the benefit of reducing disposable income and thus aggregate demand while preserving the ownership of that income.

Since there is no impediment to a bank changing a variable interest rate when allowed by a contract, mortgage holders will still be impacted, but the expected benefit of spreading the response to inflation across all households is a more effective and quicker influence causing decreasing inflation. Revenue initiatives mean the government can provide targeted cost-of-living relief.

Combined, the temporary increases in the GST and/or superannuation contributions, and the increase in interest payments by mortgage holders spreads the policy response across all consumers in proportion to their exposure to rising prices and interest rates.

There needs to be some statutory authority in the Treasury portfolio not subject to political influence making the decision to activate the temporary increases in GST and/or superannuation payments. There also needs to be some trigger event.

This trigger would be some value of the inflation policy price index above a threshold for multiple months, making allowances for price increases caused by rest-of-world events, short-term conditions and other sources of price increase consumers and businesses have absolutely no influence over.

The temporary increases and the targeted cost-of-living relief would need to be defined precisely: e.g. not less than six months, no longer than twelve months, with no extension and no repeat for twelve months; fully recoverable payments, the value of payments calculated not to over compensate consumers

This authority would decide whether targeted relief should be supply-side, demand-side or used to maintain the real interest rate (less any existing interest rate premium) paid to banks (thus helping mortgage holders), or a mix of all.

This authority would take expert advice as appropriate. This authority would be required to be independent, transparent, predictable, consistent and to provide clear communication.

Summary

Existing RBA inflation targeting policy produces economic and socially suboptimal results. Thirty-five per cent of households are burdened with the responsibility to fix an economic problem they did not create. The RBA policy is based more on subjective statements than facts. There are better policy options. The basis for one option is a national taxation policy funding targeted cost-of-living relief, and using temporary increases in the GST and/or superannuation payments to reduce inflation. A statutory authority of employee, employer and government representatives would administer this policy.

Sources

Australian Bureau of Statistics, Australian National Accounts. Retrieved from https://www.abs.gov.au/statistics/economy/national-accounts/australian-national-accounts-national-income-expenditure-and-product

Australian Bureau of Statistics, Consumer Price Index, Australia. Retrieved from https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/consumer-price-index-australia

Australian Government, The Treasury (2021) Estimating the NAIRU in Australia. Retrieved from https://treasury.gov.au/publication/p2021-164397

Federal Reserve Bank of Chicago, The Recent Steepening of Phillips Curves (Chicago Fed Letter No. 475, 2023). Retrieved from https://www.chicagofed.org/publications/chicago-fed-letter/2023/475

Keen, S. (2022). The New Economics: A Manifesto. Polity Press.

Mitchell, W., Wray, L.R. and Watts, M. (2019) Macroeconomics. London: Red Globe Press an imprint of Springer Nature Limited.

Obstfeld, Maurice. Natural and Neutral Real Interest Rates: Past and Future | IMF Economic Review | Springer Nature Link. IMF Economic Review (New York) 73 (June 2025): 53. Retrieved from https://doi.org/10.1057/s41308-025-00276-z.

Reserve Bank of Australia, Agreement on Framework for Monetary Policy. Retrieved from https://www.rba.gov.au/monetary-policy/framework/

Reserve Bank of Australia, Australia’s Inflation Target. Retrieved from https://www.rba.gov.au/education/resources/explainers/australias-inflation-target.html

Reserve Bank of Australia, The Non-Accelerating Inflation Rate of Unemployment. Retrieved from https://www.rba.gov.au/education/resources/explainers/nairu.html

Reserve Bank of Australia. 2019. “Watching the Invisibles | Speeches.” June 12. Retrieved from https://www.rba.gov.au/speeches/2019/sp-ag-2019-06-12-2.html.

Ruberl, H. et al. (2021) “Estimating the NAIRU in Australia,” Treasury Working Paper [Preprint], (2021–01). Retrieved from https://treasury.gov.au/publication/p2021-164397.

United Nations (1948) United Nations Declaration of Human Rights. United Nations General Assembly, 10 December 1948, Retrieved from https://www.un.org/en/about-us/universal-declaration-of-human-rights

ENDNOTES

- The term ‘budget constraint’ means that the agent (government or non-government) is spending (trying to spend) money they do not have or cannot afford. (Broadley, the present value of revenue equals the present value of expenditure. Specifically for a government, the present value of debt cannot be positive – future debt pays for current debt.) Under the ‘budget constraint’ conditions government spending will ‘crowd out’ private consumption and investment.

- Sources: Unemployment rate, ‘Persons; Seasonally Adjusted’ A84423050A from 62002001.xlsx, Table 1. Labour force status by Sex, Australia – Trend, Seasonally Adjusted and Original. Per cent change from the corresponding quarter of the previous year of A3604509L CPI ‘Trimmed Mean, Australia, Seasonally Adjusted’ in 64010Appendix1a.xlsx. Appendix 1a. A three-month average of the RBA series FIRMMCRT in F1.1 Interest Rates and Yields – Money Market). The Spearman’s correlation coefficients for the OCR and the TM for the same period and for four and six lagged periods, though not the best statistical test for this data, are 0.355, 0.410 and 0.390. This suggests, as intuitively expected, the OCR and TM move together. Correlation is not evidence of causation.

- Sources: Unemployment rate, ‘Persons; Seasonally Adjusted’ A84423050A from 62002001.xlsx, Table 1. Labour force status by Sex, Australia – Trend, Seasonally Adjusted and Original. Underutilisation rate, ‘Persons; Seasonally Adjusted’ A85255726K from Table X28. Underutilised persons by State and Territory and Sex – Trend, Seasonally Adjusted and Original. NAIRU, Australian NAIRU Dashboard, ‘NAIRU_aena.csv’ from https://github.com/igross/nairu/tree/main/docs/data.

- This trade-off cannot be between domestic unemployment and international prices, or government fees and charges, regulated prices, seasonal price changes, or any price inelastic to demand.

- Sources: Compensation of employees – Wages and salaries, Seasonally Adjusted, A2303355A and Total corporations; Gross operating surplus, Seasonally Adjusted, A2303369R from 5206007_Income_from_GDP.xlsx, Table 7, Income from Gross Domestic Product (GDP), Current prices.

- Assuming the distribution of consumers and income distribution is evenly spread across households. A policy could compensate mortgage holders by distorting the housing market to produce large capital gains, but that would be a Ponzi scheme with bad outcomes.

- Source: GDP per capita: Chain volume measures – Percentage changes, Seasonally Adjusted, A2304372W from 5206001.xlsx, Table 1. Key National Accounts Aggregates.

- The term ‘fiat – it is done’ comes from the Latin verb fio – to do. (Fiat money cannot be compared to the stator issued by Alexander the Great, the florin issued by the de Medici bankers or any money exchangeable for precious metal.) The increased substitution of electronic for cash money transactions has implications for fiscal and monetary policy not connected to fiat money. All expenditure of the Australian Government involves creating fiat money, as does loans made by banks. When the budget is in deficit (an increase in private sector bank deposits is greater than taxation that decreased private sector bank deposits) there is a net increase in private sector financial assets. Conversely, when the budget is in surplus there is a net decrease in private sector financial assets. You can test the claim that the repayment of private sector debt destroys money. When you borrow from a bank (a liability of the bank) the account balance becomes zero when the loan is fully repaid. You can test the claim that banks create money by recognising your bank account balance does not inexplicably decrease when some other customer takes out a mortgage.

Use of AI Declaration

AI tools were not used to check spelling, grammar, style or provide content.

About the Author

Robert Bibo BEc GradCertMgt worked at the Australian Bureau of Statistics from 1985 to 2009 in the National Accounts and Labour Force teams.

Labels: monetary policy, fiscal policy, inflation, consumer price index, modern monetary theory, heterodox economics.